We're on the cusp of a new year and it's a great time to make some changes in how you handle money.

If you're the kind of person who can't seem to rack up any savings, you've probably just been trying to bite off more than you can chew.

Everybody can save money. It's just a matter of finding the money to save in your life and then making it a priority. We'll help you on both counts!

Read more: 29 tactics for living alone without breaking the bank

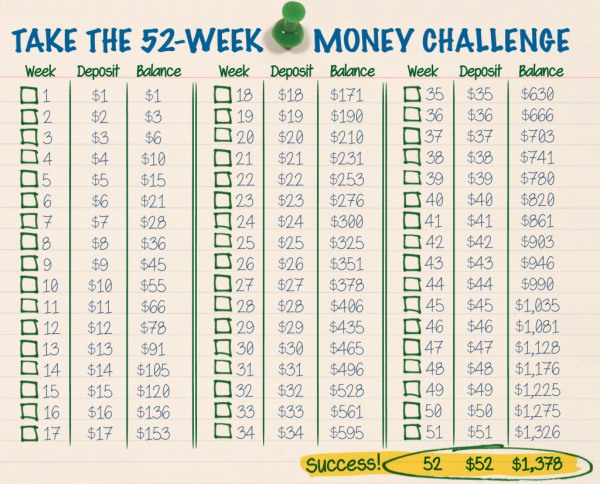

Introducing the 52-week money challenge

This chart below from The Budgetnista Blog introduces the idea of micro-savings. It all starts with socking away just $1 during the first week of January. Everybody can do that, right?

Then during the second week, you save $2. And during the third week you save $3, and on and on…

If you keep upping your savings rate by just one additional dollar a week, you'll have nearly $1,400 by the end of the year!

Sounds easy, right? Well, the devil is in the details. While it might be easy to stash away a few bucks early in the year, how about when you get toward the middle and end of the year? You'll have to come up with anywhere from $100 to several hundred dollars on a monthly basis.

But don't despair…it is possible! Here are 9 ways to reduce your bills or create more money in your life so you can successfully complete the 52-week money challenge in 2017!

1. Locate missing and unclaimed money in your name.

Simply go to MissingMoney.com and punch in your name to do a database search of available unclaimed funds across all states. Please note that not every single state participates. If you live in a state that doesn't participate with this free site, there's one more option for you: Unclaimed.org. This website is a clearinghouse for the National Association of Unclaimed Property Administrators.

Finally, maybe a grandparent bought you a savings bond when you were born and it's been lost over the years. Here's how you can track down lost savings bonds and get your money!

2. Lower your student loan payment.

Student loans are a burden for many people both young and old. Fortunately, there are ways to refinance your student loans, get on a better repayment plan or even possibly qualify for student loan forgiveness based on your choice of career! Just think about the money you could save…

3. Never buy an extended warranty on electronics.

When you're buying your next gadget, you know you'll get the pitch: Would you like to buy the extended warranty on that?

According to Consumer Reports, electronics seldom fail. In fact, TVs fail at only a 3% rate in the first four years of ownership. Why would anyone buy a warranty when you have a 97% that your TV will work for numerous years?

And here's a little known tip: Many credit cards will double the manufacturer's original warranty up to one additional year if you use them to make your purchase. That's how you approximate getting an extended warranty for free!

4. Go no contract for cell service.

It seems like every week there's a new price point being set in the telecommunications world. Did you know that's it's now entirely possible to get free phone service that will meet your needs if you're a light volume data user? No worries if you need more data; you too can save a bundle by making the switch to a low-cost carrier and still get all the data you need!

Read more: Best cell phone plans and deals for 2016

5. Reduce your withholding.

Do you get a tax refund every year? That means you've made an interest-free loan to the government and your money has been working for them — not you — all year long.

People try to justify their tax refunds by saying it's a way to force themselves to save money. Truth is, there may be a better way to accomplish the goal: Let's say you typically get a refund of $1,200 every year. Try reducing your withholding at work by $100 a month and have your bank or credit union automatically transfer that $100 each month into a savings account.

You never see the money, so you never miss it. But the end result is that you'll build your savings and earn interest all year long. Use the IRS Withholding Calculator to avoid having too much or too little federal income tax withheld from your pay. Then talk to your HR department at work to put your plan in action.

6. Stop throwing money away on expensive razors.

Every one has to shave, right? If razors take up too big a chunk of your budget, here's a little secret that will save you big bucks: Razor blades degrade much faster when they're left wet. If you either blot your razor dry on a towel after use or maybe use a hair dryer to dry it, you'll radically extend the life of the blade.

Clark himself is famous for taking a 17-cent disposable razor that he uses everyday and making it last for 12 months by using the blotting method!

7. Raise the deductible on your insurance.

The typical auto insurance customer can save up to $500 a year by bumping their deductible up from $250 to $500. That savings jumps on average to $1,000 annually if you make the leap to a $1,000 deductible.

By raising your deductible, you'll pay less in premiums, but more importantly, you'll reduce the risk that your insurer will cancel your coverage because you made too many claims. In particular, homeowners insurance can be used only in the case of a catastrophic loss. It's a "use it and lose it" proposition.

One final word about car insurance. If you have an old car that's of little value, it may be time to have liability only (not collision and comprehensive) on your policy if the cost of full coverage is greater than 10% annually of the car's value. You can determine your vehicle's value at KBB.com, NADA.com or Edmunds.com.

Read more: Best home insurers and Best auto insurers

8. Check all of your monthly statements line-by-line.

Too often, people just get bills of all kinds charged to their credit card and never see a statement. Don't be one of them! Get hold of those monthly statements and scrutinize them line-by-line.

Cell phone bills can be almost impossible to understand, making phony cram charges a real possibility. Look for line items with deceptive terms such as "Premium Content" or "Direct Bill Charge" (sometimes referred to as "DBC" on your bill.) If it's something you didn't agree to, call up your provider and get your money back.

9. Get help paying for specialty medications.

What do you do if you have an illness that requires special medicine and you can't afford it despite having insurance? One pharmaceutical executive turned philanthropist has set up a charity called TheAssistanceFund.org to provide co-pay assistance that can make the difference between life and death for some patients.

This non-profit helps pay for some medications by footing a significant amount of the out-of-pocket for insured patients. Best of all, TheAssistanceFund.org tries to approve people for assistance within 24 hours because they know time is of the essence.

Big investments start with small steps

-

Here are the best Walmart deals happening now!

-

16 of Clark Howard’s favorite deals

-

The best deals at Amazon right now!

-

125+ of the most useful items that can make life easier

-

18 eco-friendly items you can reuse instead of buying over and over

-

The best deals of the Lowe’s Spring Fest Sale!

-

The best deals of The Home Depot’s Spring Black Friday Sale

-

The best deals on grills right now

-

The best deals on laptops right now